Views: 36

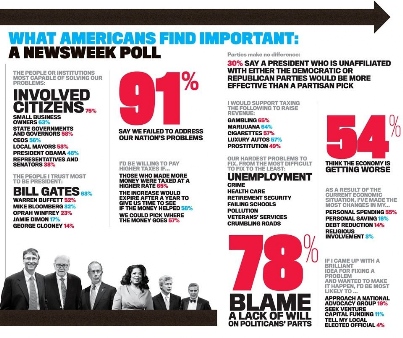

According to a recent poll conducted by Newsweek, 91% of Americans say their system failed to address the country's problems; 75% of them think "involved citizens" are the key (vs 48% picking Obama); and 63% trust Bill Gates to be their president!

Source: http://www.thedailybeast.com/newsweek/2011/09/11/what-americans-find-important-a-newsweek-poll.html

Do you really think the most "liberal and democratic" nation in the world has a solution to our problems? Talk about their Universal Values. Thank you very much, I'd rather have my Giacosa red label.

Perhaps the experts should know better. When Newsweek asked three Nobel economists to share their thoughts on America's future, what went wrong, and what can be done to fix things. These are their views about:

The Road Ahead

Strangely, all that I read is "Dead End Alley".

Sources:

http://www.thedailybeast.com/newsweek/2011/08/14/edmund-phelps-entitlements-endanger-u-s-economy.html.html

http://www.thedailybeast.com/newsweek/2011/08/15/vernon-l-smith-insolvency-policy-and-economic-stress.html.html

http://www.thedailybeast.com/newsweek/2011/08/15/michael-spence-will-the-west-stabilize-and-grow-again.html.html

#1. The Monumental Fiscal Challenge

by Edmund S. Phelps — a 2006 Nobel laureate in economics, director of the Center on Capitalism and Society at Columbia University and author of Rewarding Work.

The latest major correction in the U.S. stock market has marked an abrupt change in economic thinking. Suddenly what used to be a minority view—a grim portrait drawn by myself and a few other observers—is widely accepted: some fundamental things are wrong with America ’s economy. But “too little money chasing too many goods”—a so-called deficiency of aggregate demand—is not one of them. A deficiency emerged last year, but the Federal Reserve’s second round of “quantitative easing” got the inflation rate almost back to the target. A third round could be fired should the inflation rate sag again. The economy’s real malfunctions are structural. When recognized, they reduce valuations of stocks, capital goods, and housing. That in turn leads to a contraction of investment activity—and hence of employment.

A big problem is that fiscal discipline was thrown to the winds after the presidencies of Ronald Reagan, George H.W. Bush, and Bill Clinton. When I first heard George W. Bush speak of “compassionate conservatism,” I braced myself for a splurge of entitlement spending. The opening shot was Medicare Part D—free pills for seniors. To enact it, Congress had to abandon its 1990s rule that any bill for new spending had to provide new tax revenues to pay for it. I warned at the time that the bill violated the principle of “fiscal neutrality”: such programs make people feel far wealthier than they are, leading to reductions in saving and domestic investment. But eventually people look to the horizon and see massive levels of public debt. Then markets get frightened, and asset prices plunge.

When Barack Obama took office after years living in the hometown of Chicago economics, I assumed he would be an economic conservative but keen on job subsidies. Instead he proposed the 2010 Medicare legislation that again threatened to increase outlays without any increase in taxes to offset them. And this July he inexplicably passed up an opportunity to cut $4 trillion in federal expenditures on the grounds that the debt deal would not tax the oil and gas industries.

These are just the highlights. Thanks to Bush’s tax tables, a working-class couple with two minor children would pay no federal tax at all on income up to about $30,000 and would pay 15 percent on additional income up to about $25,000. Housing benefits, food stamps, and Medicaid might easily exceed the federal tax on a $50,000 income. The middle class gets off lightly too. The federal tax on $85,000 would be about $10,000. In effect, the bottom half of America ’s economy appears to be using its voting power to tax the top half.

That’s bad government. There would be plenty of justification to raise revenues in order to subsidize businesses that employ low-wage workers. But there can be no justification for pandering to the economy’s entire bottom half merely to attract its votes.

What makes the situation all the more unbelievable is that only 10 years ago it wasn’t like this. Expressed as percentages of GDP, America ’s total federal outlay took off like a rocket in 2002, but federal revenue has declined steadily. Mary Meeker at the financial firm KPCB estimated earlier this year that the present value of America ’s existing entitlements has soared to $66 trillion: $35 trillion for Medicaid, $23 trillion for Medicare, and $8 trillion for Social Security. And we can’t expect to “grow out” of this mountain; most signs suggest we’re headed for years of slower innovation and reduced borrowing and lending—and hence slower growth.

In that case, how can Washington keep its commitments? Some economists have suggested “restructuring” the country’s public debt—in effect, a default, which would likely cause a draconian downgrade of America ’s credit. Or we could “restructure” the entitlements, as former Fed chairman Alan Greenspan has suggested—also a default of sorts. Maybe a little chiseling is inevitable, but many Americans are counting on their entitlements in retirement. A major retreat from these commitments would be disgraceful.

The best solution of a bad lot is to boost revenues. Republicans can agree to cancel the free ride of the middle class. Democrats can end the free ride of the working class, but that will make subsidies to business for low-wage employment more necessary than ever. Both parties can agree to a value-added tax. If these changes are phased in gradually, they will not stop a recovery. The main cost of fiscal responsibility will not be jobs lost. Instead, it will be a setback in the rise of paychecks, profits, and wealth. Entitlements have to come from somewhere.

We can only hope Congress learns that lesson before it enacts any more.

#2. Insolvency, Policy, and Economic Stress

by Vernon L. Smith — a 2002 Nobel economics laureate, holds Chapman University’s Argyros Chair in Finance and Economics

Whether or not America is facing a double-dip recession, the country has already entered a double-dip growth recession as measured against the past century’s 3 percent rate of expansion. U.S. securities markets, nearly always behind the curve, have gone into a state of panicky volatility. The deficit-stimulus policies of presidents Bush and Obama have failed: the costs have far exceeded the benefits. And ordinary Americans have grown suspicious of economic experts—as well they should be.

Why is the economy stuck? The only empirical model we have for the current crisis is the Great Depression, whose severity has long been attributed to the Federal Reserve’s failure to provide desperately needed liquidity to the banks. With that conventional explanation in mind, Fed chairman Ben Bernanke set out in August 2007 to remedy the current financial crisis by injecting temporary cash into the banking system.

It didn’t work: the banks, laden with bad loans, faced outsize insolvency problems, not just a shortage of liquid funds. When Bernanke figured out the real problem, he lifted more than $1 trillion in overvalued loans from the balance sheets of U.S. banks, a move that may have saved us from a second Great Depression. Between 1930 and 1933, the unemployment rate reached as high as 25 percent, where from 2008 until now the rate has held at 9 or 10 percent. All the same, we still can’t know the full consequences of Bernanke’s unprecedented intervention—it may have just stretched the pain further into the future. In that case, Bernanke has only moved us to a different circle of hell.

In my opinion, the onset of the Great Recession in 2007 and 2008 was a twin of the 1929–30 balance-sheet crisis that ushered in the Great Depression. In both cases the problem was insolvency, not just a shortage of liquidity. The credit-fueled housing boom of the 1920s explains the bank crisis that followed. Back then, 85 percent of commercial-bank mortgages were for terms of only three or four years and were not fully amortized, ending instead with balloon payments that usually required refinancing. That financial juggling act ended in 1929, resulting in the crash, and household insolvency immediately spilled into the banking system. The deleveraging process and its economic consequences dragged on for the entire decade of the 1930s.

How long will it take to climb out of the hole this time? The trouble is that Bernanke’s stimulus spending was a blunderbuss. It didn’t address the need to restore the damaged balance sheets of banks and households, and without such repairs, businesses and consumers will be obliged to keep paying down debt rather than hiring and spending, while banks will concentrate on piling up cash reserves in order to cover bad loans instead of making new loans to get the economy up and running again. Troubled assets were removed from the banks’ books at face value, to be replaced by reserves on which the Fed pays interest to the banks, rewarding them for not making loans. Meanwhile, many struggling homeowners had their mortgage payments reduced by lengthening their loans or reducing interest rates—not by reducing principal to realign their debt with home values.

But without balance-sheet restructuring, such adjustments only extend America ’s bullet-biting into the indefinite future. The painfully slow process of deleveraging continues to handicap the prospect of recovery. The Fed rescue may have boosted spirits at financial institutions, but it’s now clear that the seemingly miraculous rebound of bank profits was an accounting artifact that took insufficient notice of sour loans. And now the window for raising private bank capital to reboot damaged balance sheets has slammed shut.

In the past four years we’ve seen all manner of egregiously mis-aimed policy actions, from the federal government’s stimulus program to Cash for Clunkers. Policymakers keep repeating the same mistake that caused the crisis in the first place: using more and more credit to move future demand into the present. This is not sustainable. It’s still not too late to refocus policy on the real problems that have disabled the economy, rather than on the secondary symptoms of the crisis. But even then, a quick recovery seems unlikely.

3. Will the West Stabilize and Grow Again?

by Michael Spence — a 2001 Nobel laureate in economics, is the author of

The Next Convergence: The Future of Economic Growth in a Multispeed World.

Coming home from my Italian vacation this year was an abrupt transition. From the calm waters of southern Sardinia , I was plunged into the global economy’s stormy seas. Financial markets were plummeting, driven by pessimistic growth forecasts in Europe and America . Investors were fleeing for safety pretty much everywhere. Systemic risk—the statistical likelihood of outright economic collapse—was rising. Yields on Italian and Spanish sovereign debt were climbing into the danger zone, threatening to fly out of control. America was on the verge of a technical default on its sovereign debt.

Weeks later, the fear in the markets is only growing worse. It comes in part from a large and still-incomplete market correction. But more than that, the policymaking bodies of Europe and the United States seem paralyzed. On both sides of the Atlantic there are unsettling similarities. In the face of very clear—and admittedly difficult—challenges to restore fiscal stability and stimulate medium- and long-term growth, government response is in various states of gridlock and denial.

In response to Washington ’s dysfunction on the debt issue, Standard & Poor’s downgraded America ’s credit rating (prematurely, in my view). Nevertheless, the markets have not abandoned U.S. bonds. For one thing, big investors like China have no practical alternative. For another, the risk still isn’t all that high. But trouble is deepening around the world. Equity prices are dropping as growth falls away or is threatened. Employment is stagnant, and policy processes are stuck. Fears of a global downturn are rising; some view it now as a near certainty. Jobs will be a major casualty, especially for the young. Even in the emerging economies, growth seems likely to suffer. Prospects for improvement seem remote.

And why has the focus of the policy debate in Washington borne so little resemblance to what most Americans seem to want? Traveling around the United States on a book tour in May and June, I spoke with many people who wanted nothing more than a coherent bipartisan plan—a plan that would focus on the future, on employment and growth. They recognized that getting there would take sacrifices. Polls suggest that many Americans share that desire. And yet in Washington the legislative process has not produced anything like that kind of consensus.

Some observers argue that Americans are looking for a solution that simply isn’t feasible. Others say the country’s philosophical disagreements over economic priorities are so large that compromise is practically impossible. Both views may contain some truth. But the real sticking point seems to be something other than the economy: the size and role of government. Fiscal stabilization is only the battleground, not the objective. Jobs and economic growth are related only tangentially to the policy debate.

There’s another problem, too, and it’s not confined to the United States . Enabled by a combination of public and private debt, much of the Western world has been living far beyond its means for at least two decades. By now the pattern has embedded itself deep in the expectations of people who have come to see it as normal. But it’s no longer sustainable.

To restore a stable pattern of inclusive growth—the kind that truly lifts all boats—the first step is to reduce the debt loads in these economies, not suddenly but systematically. That alone won’t be enough. Consumption and government services will have to be reset downward, replaced by public and private investment that is funded by domestic saving. The path we’ve been on is blocked; we need to take a few steps backward to be able to go forward again. Nevertheless, this harsh truth has not yet been accepted by governments or electorates. Instead we appear to be clutching at our past standards of living, hoping for a vigorous but delayed cyclical recovery. The unemployed are the ones paying for this strategy.

The world is at a crossroads, with popular expectations diverging from reality. With luck, our policymakers may become more bold and focused, leading toward a more balanced and durable growth pattern. That is the hope. Still, it could go the other way—bickering our way into a relatively stagnant future, fraught with political and social conflict and inequities.

I am no economist but I don't need to be one to understand what really went wrong. It is just common sense that if one cannot afford to spend, he or she would tighten the belt and save up hard. But for the Americans, they work on reverse logic by pumping extra money into "everyone's" wallet to stimulate spending. It might work in the very short run… but the fact that when debts remained unpaid, it doesn't matter who owns them, they will still remain unpaid. The ability of Fed's QE rests on their ability to print money… but not for long.

[版主回覆09/23/2011 08:58:00]Are you advocating a return to pre-industrial times when everything is paid by cash or even bartering? Would you buy a property with cash even if you have enough cash? Sorry, the world economy has been built on sand (read "credit") long before you and me were born.

But to return to the question of what went wrong about sovereign debts, we now have the Nobel laureates' consensus that the "democratic" process encourages a lapse of public responsibilities: the politicians try to give what people "want" by taking the voters' money to buy a can of beer for the working class, and a bottle of cheap Bordeaux for the middle class. The fat cats drink Lafite and pop Cristal. When crunch time comes, the fat cats withdraw money from the table, and both the middle class and working class lose their jobs. Other politicians will come along and say they will be the next saviors, so just wait in line in the polling station.

That's Hong Kong too. They say democracy is the least good system, so be happy and live and die for it.

But no no, I'd rather have my Giacosa red label.